The era of US exceptionalism is fading, and the US dollar’s (USD) status as a safe-haven currency is facing growing skepticism. Central banks are gradually diversifying away from the USD reserves, while markets are increasingly concerned about America’s fiscal profligacy. This has strengthened the view that the USD is entering a phase of structural depreciation, further reinforced by the current administration’s apparent preference for a weaker dollar.

Against this backdrop, there is a growing misconception that a weaker dollar will automatically translate into a stronger Indian rupee (INR). While we broadly agree with the view of a softer dollar over the long term, we believe the impact on the INR warrants a more nuanced discussion. A weaker dollar does not necessarily equate to INR appreciation against the USD.

Relative Purchasing Power Parity (RPPP) provides a valuable framework for analyzing the USD-INR relationship. RPPP is based on the principle that, over the long term, exchange rates adjust to offset inflation differentials between countries, thereby preserving relative purchasing power. This implies that currencies of countries with higher inflation tend to depreciate relative to those with lower inflation, so that identical goods should cost the same globally.

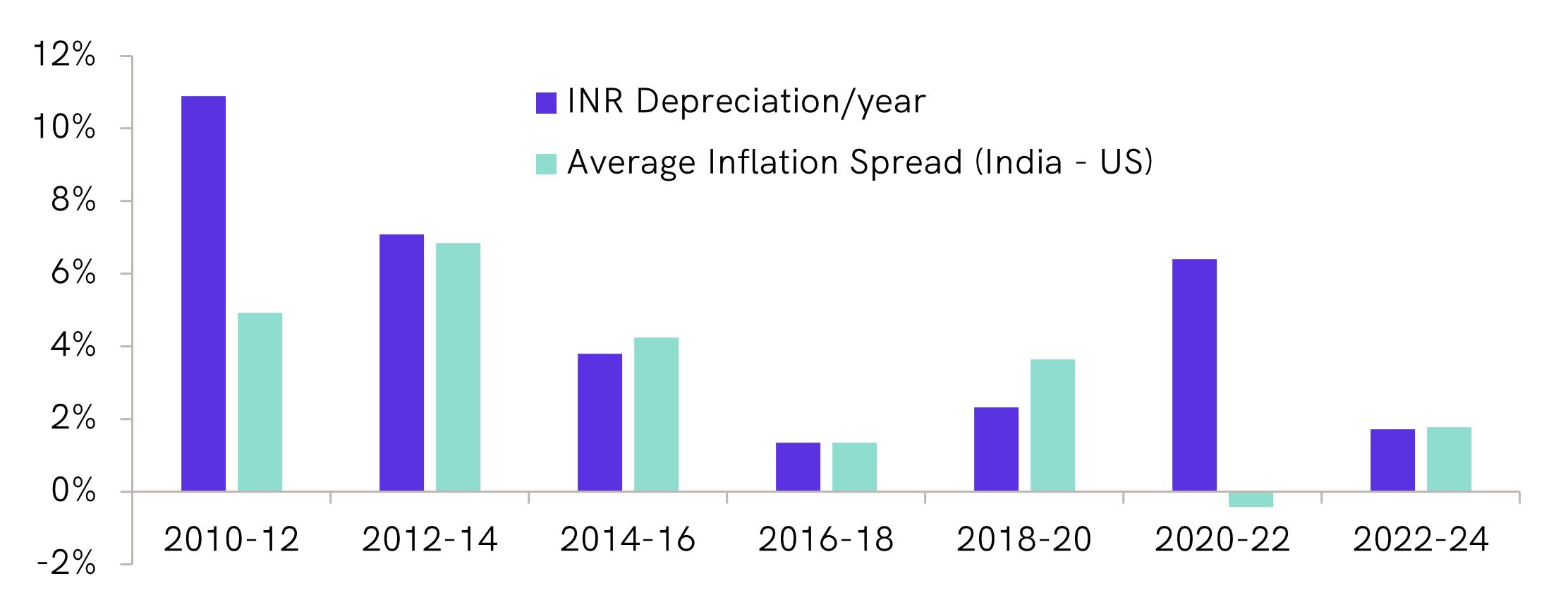

Admittedly, RPPP has its limitations. It does not hold uniformly across periods and ignores critical factors like productivity differences and capital flow dynamics. However, historical trends broadly support the directional validity of RPPP for India (Chart 1).

Chart 1: Inflation Spread Vs INR Depreciation

Source: Bloomberg, FRED, MOSPI, 360 ONE Research

Source: Bloomberg, FRED, MOSPI, 360 ONE Research

Between 2010 and 2018, a narrowing inflation spread coincided with slower INR depreciation. During 2018–2020, a widening inflation differential aligned with faster depreciation. However, anomalies like 2020–2022 remind us that global factors (COVID-driven risk aversion, oil shocks) can override inflation trends in the short term. During 2022–2024, depreciation was broadly aligned with the inflation differential.

Therefore, under the reasonable assumption that India and the US maintain inflation rates near their respective targets of 4% and 2%, the inflation differential would hover around 2%, implying a gradual depreciation of the INR against the USD over the medium to long term.

Another crucial, but often overlooked, factor is the RBI’s response function. While the RBI maintains that its FX interventions are solely intended to curb volatility, we observe a tendency to be more proactive in resisting appreciation. It actively accumulates reserves during capital inflows, when appreciation pressures typically build, while allowing depreciation to unfold more gradually during episodes of capital outflows. This approach effectively caps INR appreciation while managing depreciation in a more controlled and orderly manner.

Additionally, while the USD’s global dominance may gradually decline, the process will likely be protracted. According to our analysis of the IMF COFER dataset, the USD still accounts for around 58% of global central bank currency reserves and remains the primary reserve currency. Periods of heavy risk-off would still trigger capital movement from riskier Emerging Market (EM), such as India, to comparatively safer USD assets, creating depreciation pressure on the EM currencies.

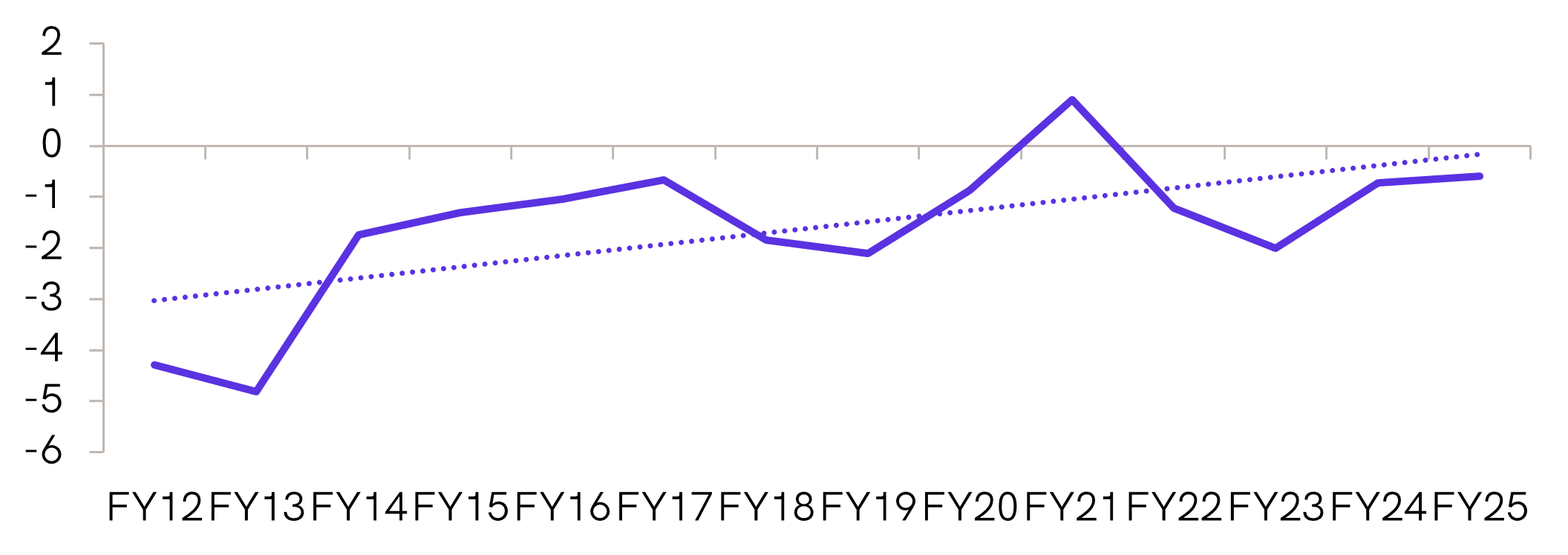

However, India’s strong macroeconomic fundamentals signal a more contained pace of currency depreciation compared to the past. Over the last decade, the country has recorded a marked improvement in its current account balance (Chart 2), while maintaining fiscal discipline and sustaining robust economic growth. This strengthening in fundamentals is further reflected in a decline in India’s risk premium relative to the US, as evidenced by narrowing interest rate differentials (Chart 3).

Chart 2: India Current Account Deficit (% of GDP)

Source: CMIE, 360 ONE Research

Source: CMIE, 360 ONE Research

Chart 3: 10-year sovereign bond yield spread: India over US

Source: Bloomberg, 360 ONE Research

Source: Bloomberg, 360 ONE Research

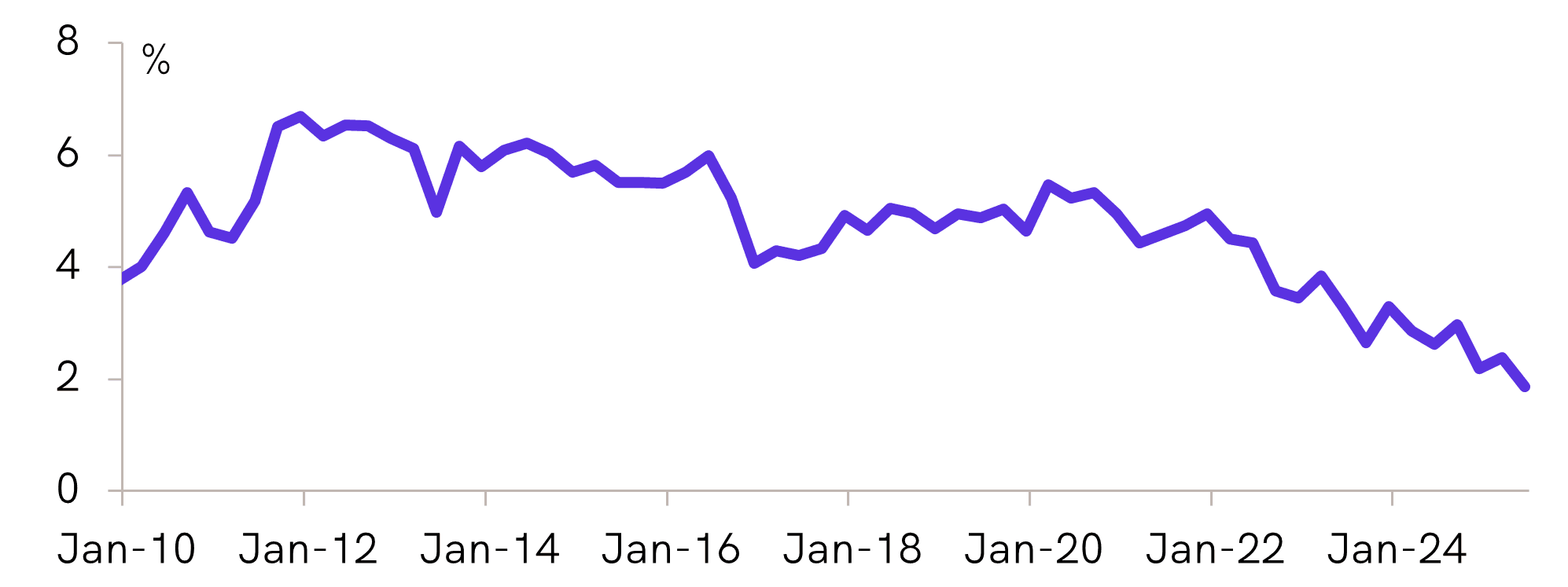

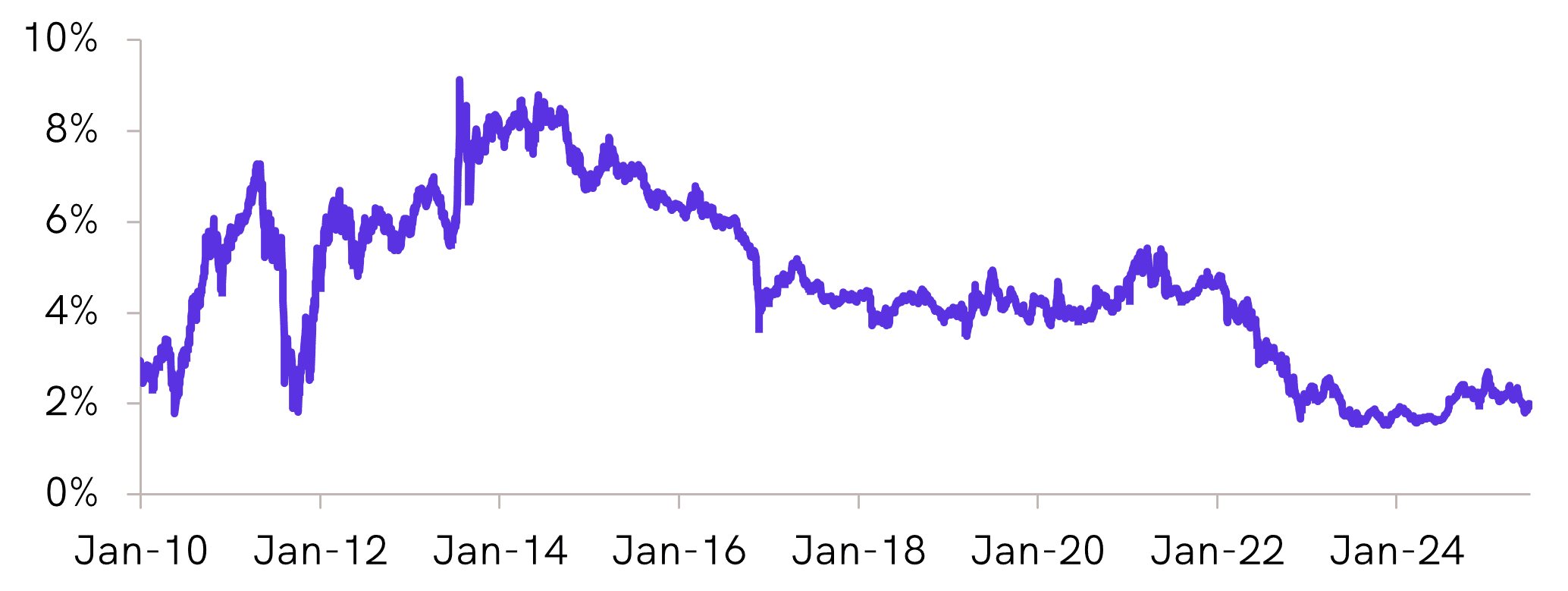

Consequently, we expect the INR to depreciate at a more moderate pace of 1.5-2.0% per annum on average, compared to the 3% annual depreciation recorded since 2010. This view is broadly consistent with the decline in the cost of hedging INR exposure, with the USDINR 12-month forward premium (Chart 4) falling from an average of 4.2% during 2017–22 to around 2.0% in 2023–2025 (till June). Moreover, the anticipated weakness in the US dollar further supports this outlook and could result in an even slower pace of INR depreciation.

Chart 4: USD/INR - 12M Forward Premium (%)

Source: Bloomberg, 360 ONE Research

Source: Bloomberg, 360 ONE Research

In summary, even if the dollar weakens against other developed market currencies, we do not expect the INR to appreciate sustainably against the USD. While brief episodes of appreciation are possible, the broader trend is likely to be a more contained pace of depreciation compared to historical norms.