The Reserve Bank of India (RBI) has introduced several measures in recent months to improve liquidity in the banking system. These steps aim to boost credit flow to the economy and support economic recovery. However, to fully grasp the impact of the RBI’s liquidity measures, it is crucial to first understand the concept of banking liquidity.

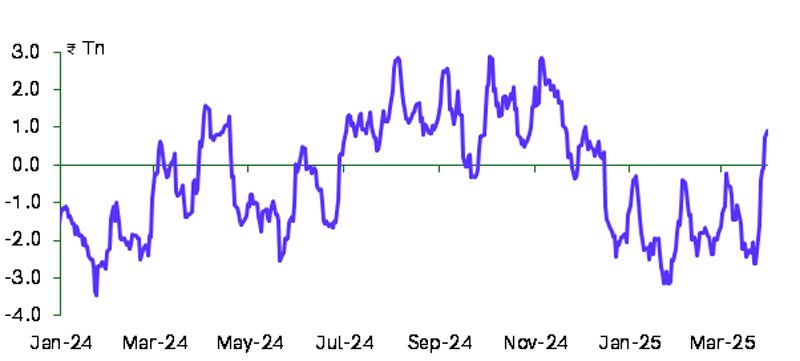

Liquidity in the banking system is measured by the net amount borrowed from or lent to the RBI. When banks are net borrowers from the RBI, liquidity is in deficit; conversely, when they lend to the RBI, liquidity is in surplus.

If banks lack sufficient funds to meet credit demand, they borrow from the RBI through the repo window to on-lend as bank credit, indicating a liquidity deficit. In contrast, when banks have excess funds, they park the surplus with the RBI through the reverse repo or standing deposit facility, signifying a liquidity surplus.

Chart 1: Banking System Liquidity - Surplus(+)/Deficit(-)

Source: RBI, 360 ONE Asset Research

Source: RBI, 360 ONE Asset Research

Key Factors Affecting Liquidity:

- Currency Demand: An increase in currency demand leads to a reduction in liquidity as people withdraw deposits from banks.

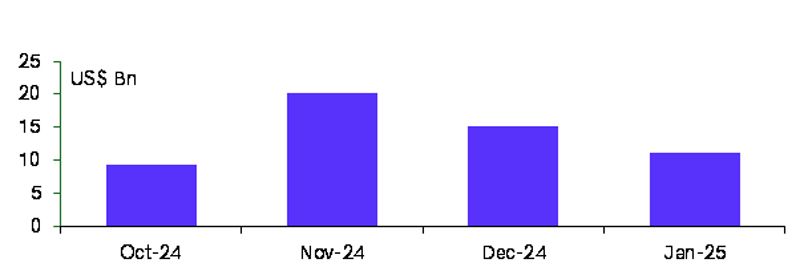

- RBI’s foreign exchange (FX) operations: These can have either a negative or positive impact on liquidity. When the RBI sells US$ from its reserves, it reduces domestic liquidity, whereas when it buys US$, it improves liquidity. The recent liquidity deficit has been driven by the RBI selling US$ to defend the currency against heavy FPI equity outflows. From October 2024 to January 2025, the RBI sold US$56 billion from its reserves, thus effectively withdrawing the same amount from the banking system.

**Chart 2:** RBI FX Operations

Source: RBI, 360 ONE Asset Research

Source: RBI, 360 ONE Asset Research

3. Government’s Cash Balance: The government's cash balance with the RBI can also impact liquidity. For example, when you pay taxes, the money is transferred from your deposit account to the government's account with the RBI, thereby reducing the banking system’s liquidity. In contrast, when the government spends, the money is transferred from the RBI’s account to the deposit accounts of employees, vendors, and others, thereby improving liquidity. Additionally, the transfer of dividends from the RBI to the government could enhance liquidity as and when the government utilises the funds.

RBI’s Liquidity Management

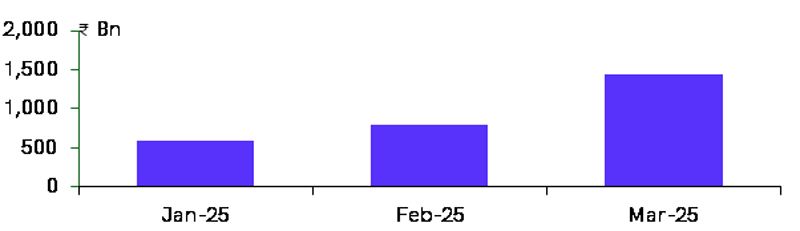

- Open Market Operations: The primary tool used by the RBI to manage liquidity is Open Market Operations (OMOs). An OMO involves the purchase or sale of government securities (G-secs) by the RBI. When the RBI purchases G-secs, it infuses liquidity into the banking system, whereas when it sells G-secs, it withdraws liquidity from the system. Since December 2024, the RBI has conducted OMO purchase auctions worth ₹2.8 trillion (~US$33.1 billion) to sterilise the impact of FX operations.

**Chart 3:** RBI OMO Purchase Operations

Source: RBI, 360 ONE Asset Research

Source: RBI, 360 ONE Asset Research

2. Cash Reserve Ratio: The RBI can also alter the Cash Reserve Ratio (CRR) to manage liquidity. An increase in the CRR leads to a reduction in liquidity, while a decrease in the CRR leads to an increase in liquidity. During the December 2024 monetary policy, the RBI announced a 50-basis-point reduction in the CRR, adding ~₹1.16 trillion (~US$13.6 billion) in liquidity.

3. FX Swaps: Additionally, the RBI can conduct FX swaps, which function similarly to the FX operations discussed above. However, as it is a swap, the transaction must be reversed at a later date. Since January 2025, the RBI has conducted US$25 billion worth of USD/INR Buy/Sell swaps to infuse liquidity into the banking system.

Implications of Surplus/Deficit Liquidity

Liquidity conditions play a pivotal role in the transmission of monetary policy to the real economy. When liquidity conditions are in sync with changes in policy benchmark interest rates, policy rate adjustments transmit more quickly to the real economy.

During a rate cut cycle, surplus liquidity ensures that banks have sufficient funding, allowing them to reduce deposit rates and, consequently, extend credit to borrowers at a lower rate. Conversely, during a rate hike cycle, tightened liquidity forces banks to pay higher interest on deposits and, in turn, charge higher interest on credit. Hence, interest rate cuts or hikes are quickly transmitted to the real economy through appropriate liquidity conditions.

The RBI initiated the rate cut cycle with a 25-bps rate cut in February 2025. However, deficit liquidity conditions will hinder the effective transmission of monetary policy to credit and deposit rates. To address this, the RBI has announced a series of measures to ease liquidity conditions.

Outlook

The RBI has initiated the rate cut cycle as the inflation outlook has improved considerably, while growth momentum remains weak. We expect the RBI to maintain a surplus in liquidity to ensure swifter transmission of interest rate cuts to deposit and credit rates. The RBI is also expected to transfer a hefty dividend of ₹2-2.5 trillion (~US$23-29 billion) in May 2025, which will gradually add to liquidity as the government spends.

We expect monetary policy easing to support a rebound in bank credit growth, which declined to 11% YoY in March 2025 from 16.5% YoY a year earlier. Improved credit availability, combined with lower borrowing costs, should help support private sector investment and consumption, providing much-needed support to the ongoing economic recovery.

Source: Reserve Bank of India

Disclaimer:

The information used towards formulating the outlook have been obtained from sources published by third parties. While such publications are believed to be reliable, the opinions expressed in this document are of personal nature. It is hereby expressly stated that, neither the AMC, its officers, the trustees, the Fund or any of their affiliates or representatives assumes any responsibility for the accuracy of such information or the views thereof. Statements/ opinions/recommendations in this communication which contain words or phrases such as “will”, “expect”, “could”, “believe” and similar expressions or variations of such expressions are “forward – looking statements”. Actual results may differ materially from those suggested by the forward-looking statements due to market risk or uncertainties. The above is only for information purposes and do not constitute any guidelines or recommendation on any course of action to be followed by the reader. Recipients of this communication should rely on information/data arising out of their own investigations. Further, 360 ONE Mutual Fund, its Sponsor, its Trustees, 360 ONE AMC, its employees, officer, Directors, etc. assume no financial liability whatsoever to the user of this document. This document is for general information purposes only and should not be construed as solicitation to invest in the Mutual Fund schemes.

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully